From Spike to Stability: Global Airfares Enter a Higher Pricing Regime in 2026

Introduction

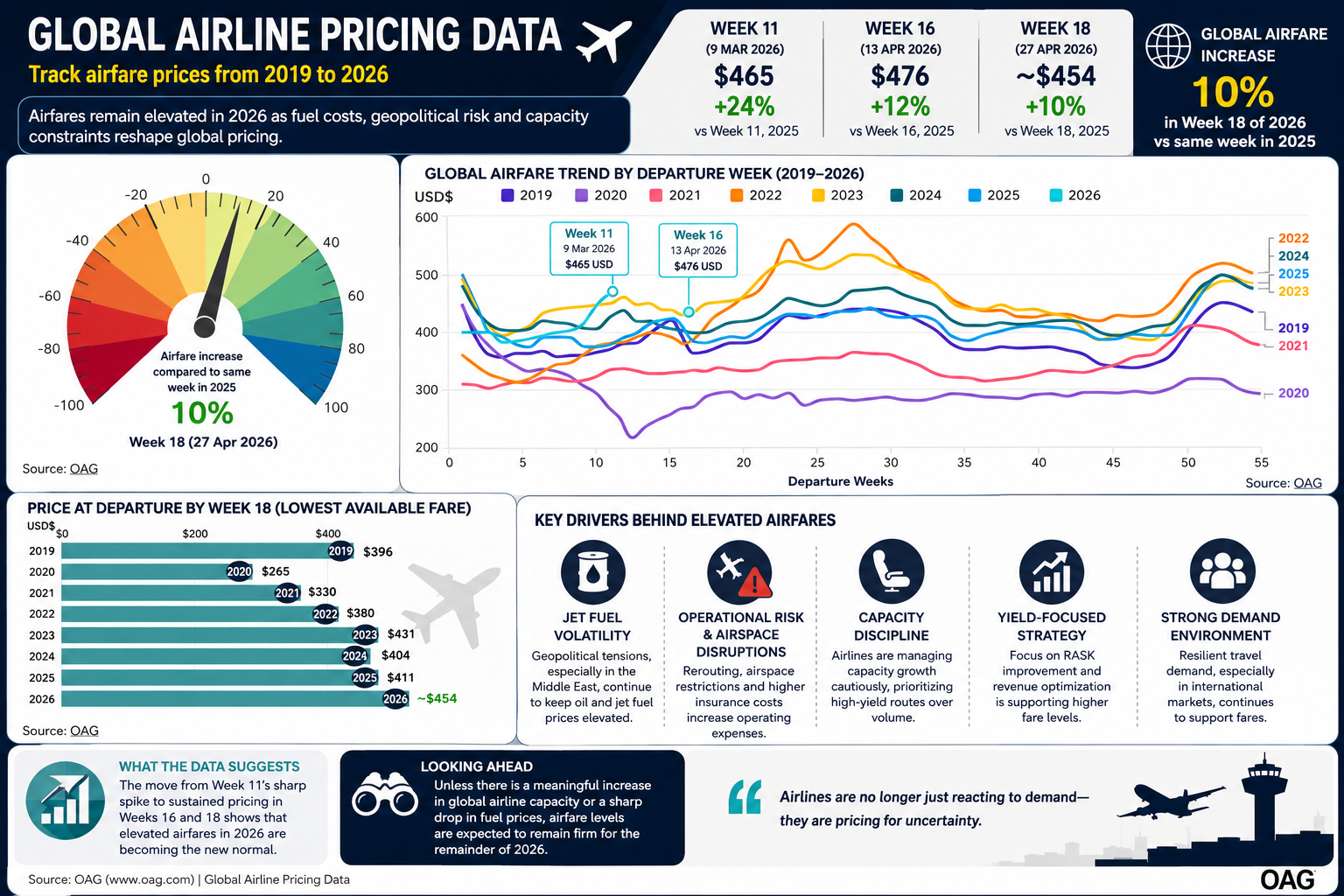

Global airline pricing in 2026 continues to reflect an increasingly fragile operating environment. What initially appeared to be a temporary airfare spike in March has now evolved into a broader trend of sustained elevated pricing across international markets.

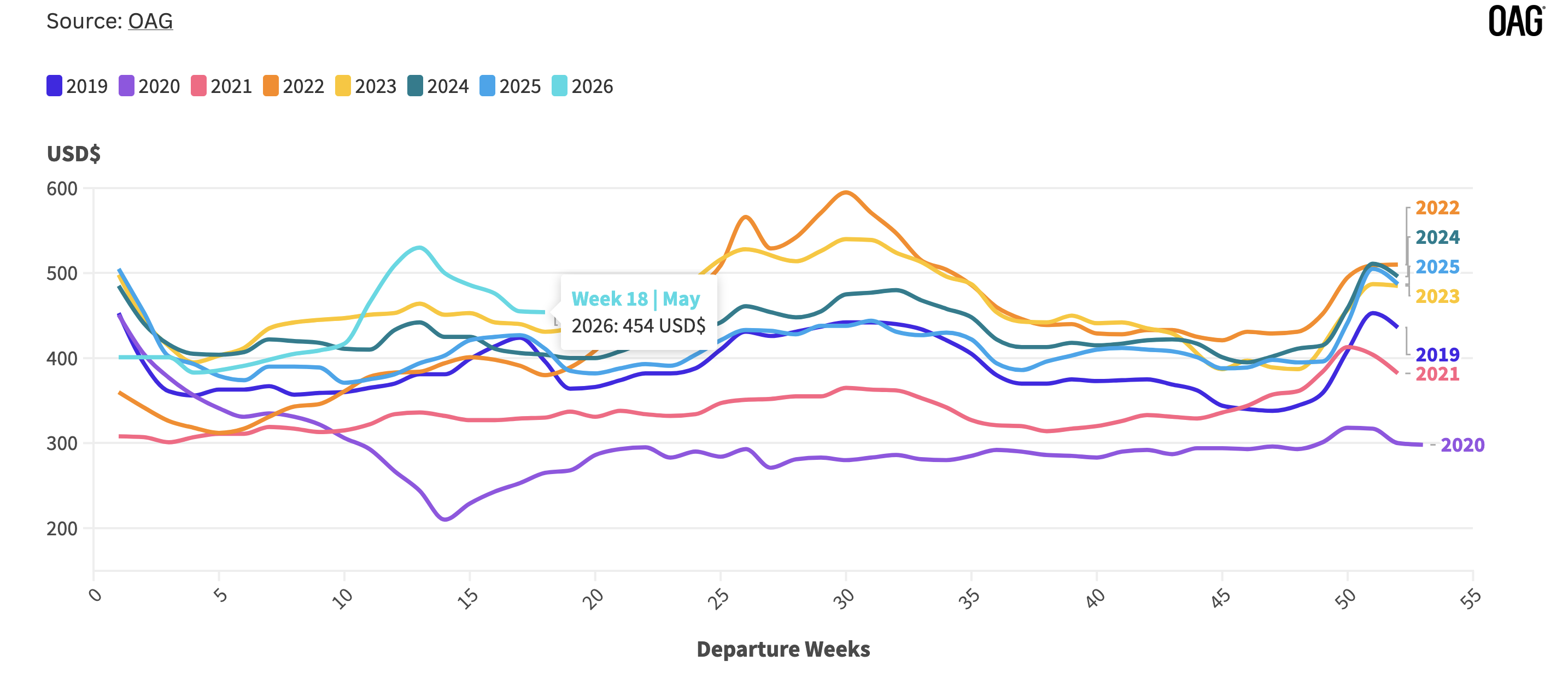

According to the latest global airfare data from OAG Airfare Insights, average lowest available airfares in Week 18 of 2026 (week commencing 27 April) remain significantly above prior-year levels, reinforcing the idea that airlines are operating under a structurally tighter supply-demand equilibrium.

The data suggests that airfare inflation is no longer being driven solely by post-pandemic demand recovery. Instead, pricing dynamics are increasingly influenced by:

- Geopolitical instability

- Jet fuel cost volatility

- Airspace and operational disruptions

- Capacity constraints

- Yield-focused network strategies

Global Airfare Trend Continues Into Week 18

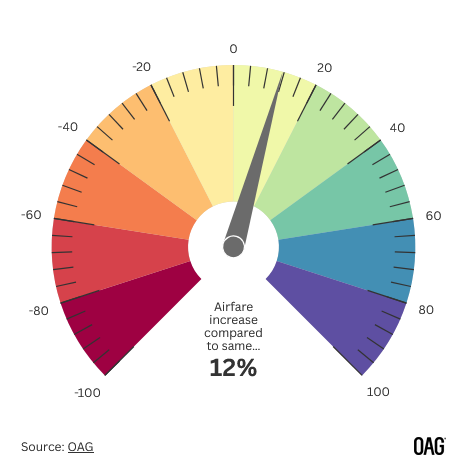

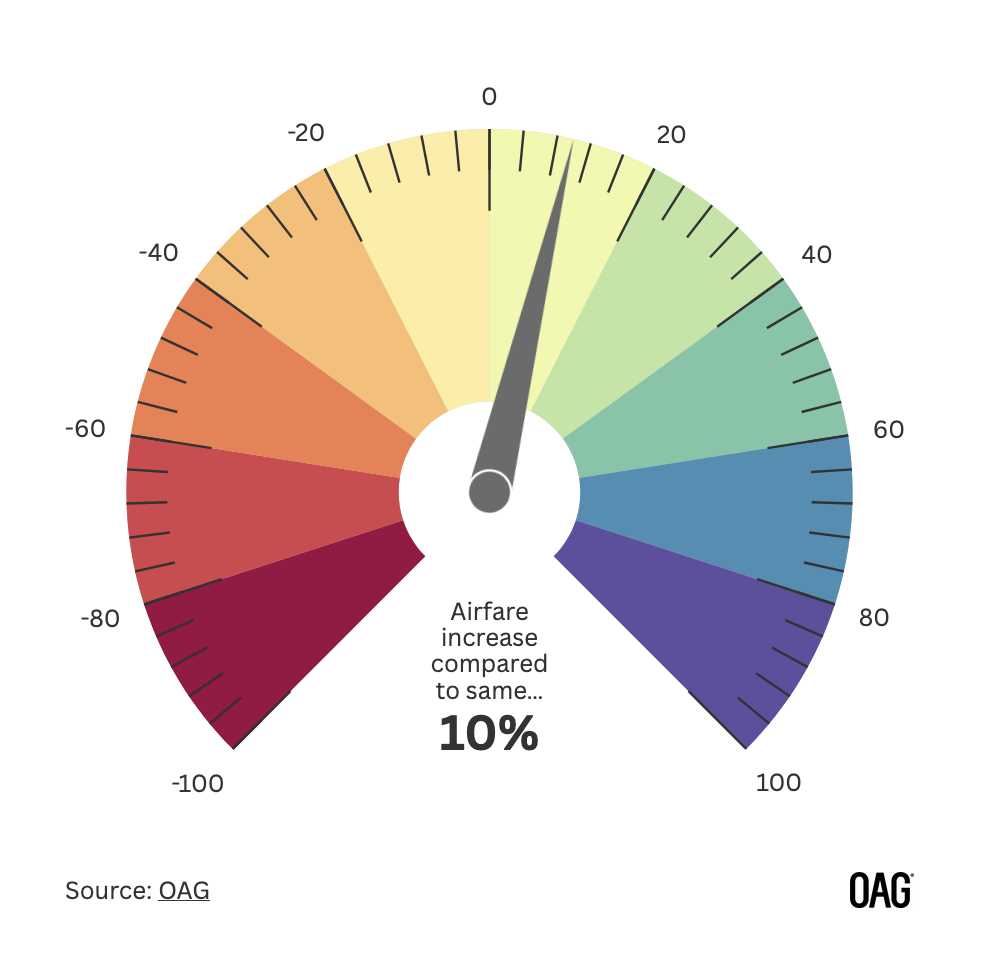

The latest OAG indicator shows that global airfares in Week 18 were approximately 10% higher than the same week in 2025.

While a 10% increase may appear moderate compared to the sharp spikes observed earlier in the year, the persistence of elevated pricing is the more important signal for the aviation industry.

This indicates that airlines have successfully maintained pricing power despite broader macroeconomic uncertainty.

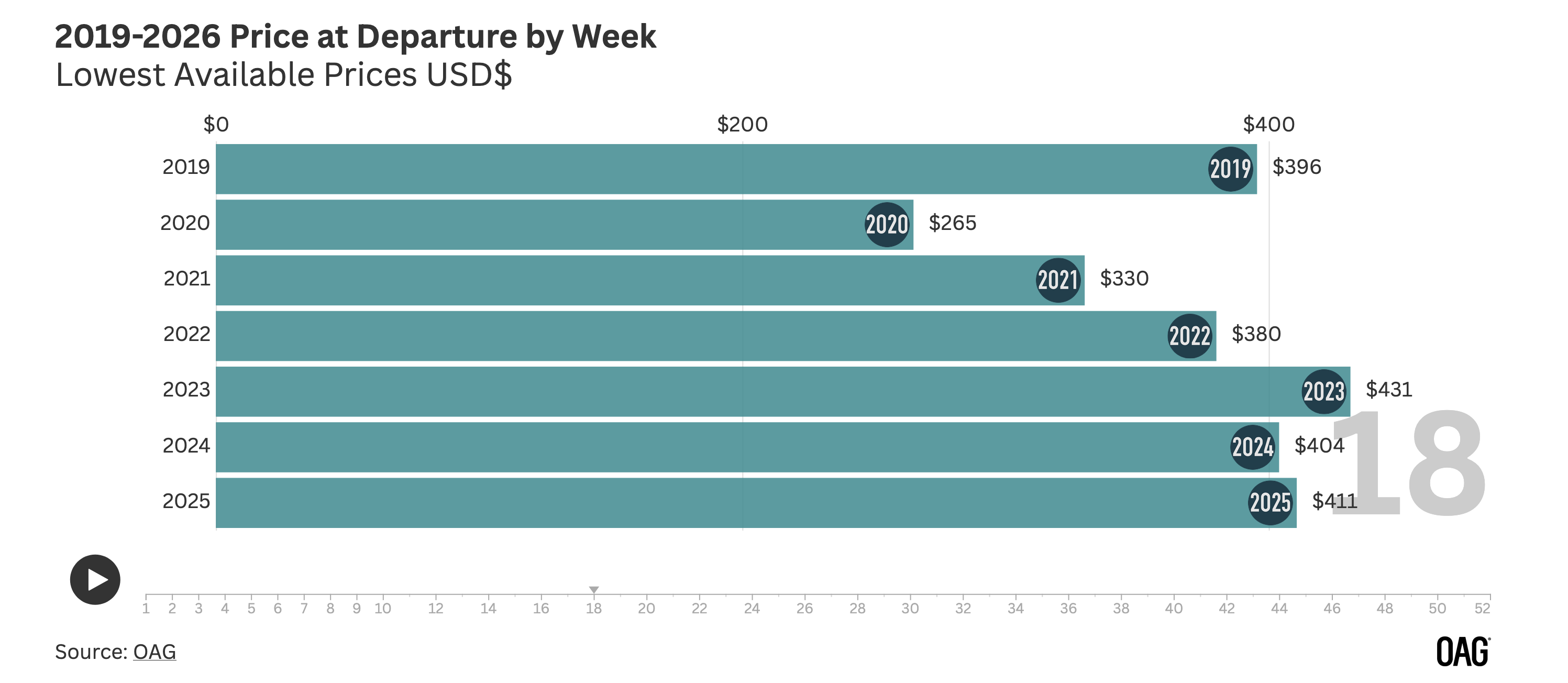

Week 18 Pricing Remains Elevated Historically

Historical airfare comparison for Week 18 highlights how pricing in 2026 remains well above pre-pandemic norms:

| Year | Week 18 Average Fare |

|---|---|

| 2019 | USD 396 |

| 2020 | USD 265 |

| 2021 | USD 330 |

| 2022 | USD 380 |

| 2023 | USD 431 |

| 2024 | USD 404 |

| 2025 | USD 411 |

| 2026 | ~USD 454 |

Compared with:

- 2019: fares are ~15% higher

- 2025: fares are ~10% higher

This confirms that elevated pricing is not merely a seasonal anomaly but part of a broader structural trend.

The Week 11 Shock Became a Week 18 Trend

Earlier in the year, Week 11 recorded one of the sharpest airfare increases of 2026, largely associated with escalating geopolitical tension involving Iran, Israel, and the United States.

At the time, many observers viewed the spike as temporary. However, by Week 16 and now Week 18, pricing levels remain consistently elevated.

This progression suggests the market has transitioned from:

Short-term fare shock → sustained high-yield environment

The persistence of higher fares reflects broader structural pressures across global aviation.

Key Drivers Behind Elevated Global Airfares

1. Jet Fuel Price Volatility

Fuel remains the largest variable cost component for airlines.

Geopolitical instability in the Middle East — particularly involving Iran-related tensions — continues to pressure oil markets and jet fuel refining margins.

Any threat to energy supply routes, especially around the Strait of Hormuz, immediately impacts airline operating economics.

Higher fuel costs translate directly into:

- Increased CASK (Cost per Available Seat Kilometer)

- Higher breakeven load factors

- Fare increases to protect margins

2. Operational Risk and Airspace Constraints

Airlines are also facing increasing operational complexity:

- Airspace restrictions

- Conflict-zone rerouting

- Longer flight paths

- Higher war-risk insurance premiums

These disruptions increase:

- Fuel burn

- Block hours

- Crew utilization costs

- Fleet scheduling inefficiencies

Even when passenger demand remains stable, these operational factors place upward pressure on ticket pricing.

3. Capacity Discipline Across the Industry

Unlike the aggressive growth cycles seen before the pandemic, airlines are now prioritizing profitability over market share expansion.

Carriers continue to:

- Limit marginal route expansion

- Delay capacity deployment

- Prioritize high-yield corridors

- Maintain strong load factors

At the same time, fleet growth remains constrained by:

- Aircraft delivery delays

- Engine maintenance backlogs

- Supply chain bottlenecks

This controlled ASK growth is helping airlines sustain elevated fare levels globally.

4. Revenue Management Has Fundamentally Changed

One of the most important structural changes since the pandemic is the industry’s shift toward:

Yield optimization rather than volume maximization

Airlines are increasingly focused on:

- RASK improvement

- Premium cabin monetization

- Dynamic pricing discipline

- Ancillary revenue enhancement

This means carriers are now more willing to preserve higher fare environments rather than stimulate demand through aggressive discounting.

What the Data Suggests for the Rest of 2026

If fuel volatility and geopolitical uncertainty continue into the second half of the year, global airfare pricing is likely to remain elevated.

Key indicators to monitor include:

- Jet fuel crack spreads

- Middle East geopolitical developments

- Airspace restrictions

- Aircraft delivery schedules

- Summer 2026 capacity growth

Unless there is a significant increase in global airline capacity, pricing pressure is expected to persist across both short-haul and long-haul markets.

Conclusion

The latest OAG data confirms that 2026 is shaping into a year where airline pricing is increasingly influenced by:

- Energy market instability

- Operational risk

- Strategic capacity control

- Structural supply limitations

The progression from the Week 11 spike to sustained pricing strength in Week 18 demonstrates that airlines are no longer merely reacting to demand recovery.

They are now pricing for uncertainty.

Source: www.OAG.com